In 2007, this man performed a very un-British coup against his former boss in what is destined to go down as the most sensational example of bad timing in the history of British politics.

Recklessly blind to the horrors that awaited him, Brown's desperation to be Prime Minister led him to hound Tony Blair out of Number 10 and claim his life's ambition at the exact height of the greatest boom in world economic history.

Then, perched atop the bust, he spectacularly failed to call an election in the autumn of 2007 at the peak of the bull market in stocks and the beginning of the greatest period of wealth destruction in modern times.

You and I are now about to be asked to vote this man back into power and legitimize him, affirm his party's fitness to govern and endorse its economic policies for another five years.

Should we?

As regular readers will know, I've never hidden my withering disdain for Gordon Brown in these columns; but if you're wondering whether my vitriol is ideologically motivated I can tell you that I'm just as queasy at the prospect of electing his opposite number. So what if I decide to fence-sit and plump for a third party? Could the consequence be even worse? Could I be 'letting the wrong lot in by the back door' or even, criminally, wasting my vote?

For me, this electoral 'eeny-meeny-miny-moe' is nothing new: in recent elections I've voted for three different parties. Shackled by our neanderthal voting system and having no class war to fight, I usually find myself voting tactically in some grubby manoevre.

But this time the choice appears stark, even binary. This time, we're told, there's an economic recovery at stake.

So the question you and I are going to have to answer to our satisfaction by May 6th, dear reader, seems dead simple: which of these meat-heads is least likely to screw up?

But does it really have to boil down to a 'least worst' contest on May 6th? If not, how are those of us without a phD or a Nobel prize supposed to judge between the competing economic arguments? Are one party's policies doomed to lead us into the abyss? Or will another's surely whisk us out of Oz and safely back to Kansas?

If you've already made up your own mind, Dorothy, pick up a stick of technicolor candy and go to the top of the class.

If not, don't despair! Take inspiration from Graham Norton and Andrew Lord Pigface's latest TV adventure. All you need do is put on your glittering ruby-red slippers, click your heels three times and join me, Toto, as we fly...

OVER THE RAINBOW...

Follow the link in the playback to 'new version' if you want to sing-a-long-a-Judy!

Ever since L. Frank Baum published his original childrens' book back in the year 1900, scholars, mythologists and psychologists have had a field day unearthing hidden meanings in the eternally popular story of The Wizard of Oz.

Well, sorry to be such a philistine, but once you've read my own interpretation I think you'll agree his meaning was pretty darned obvious...

~~~~~~~~

~~~~~~~~~~~~~~~

~~~~~~~~~

~~~~~~~~~

~~~~~~

Swept away to Oz in a monstrous cyclone, simple farm girl Dorothy (along with her trusty dog Toto) finds herself stranded in a strange and scary place controlled by the Wicked Witches of the East and West...

Dorothy longs to return home to Kansas. But she's told that the only way she can is to place her trust in a great and all-powerful Wizard, who lives in a great big castle in the Emerald City, at the end of a Yellow Brick Road...

Glinda the Good Witch tells her that if she genuflects before and believes whole-heartedly in the power of the all-powerful Wizard, he will help her to return home. Wearing a pair of magic ruby-red slippers to protect her, she skips off down the Yellow Brick Road...

Glinda the Good Witch tells her that if she genuflects before and believes whole-heartedly in the power of the all-powerful Wizard, he will help her to return home. Wearing a pair of magic ruby-red slippers to protect her, she skips off down the Yellow Brick Road... It's not long before she picks up three weird and whacky companions who are also seeking the power of the Wizard: a Scarecrow in dire need of a brain...

A Tin Man who yearns to have a heart...

And a great big growly Lion (who's just a wee timorous beastie at heart and really longs to find some...)

Despite attempts to thwart their progress by the Wicked Witch of the West, the foursome finally come before the Wizard - who seems curiously reluctant to see them. He thunders and puffs, blaming all the troubles of the land on the wickedness of the Wicked Witch. But he does promise that, if the Witch is stripped of her powers, he will be able to grant them their hearts' desires...

Off they go into battle with the forces of the Wicked Witch, who, after much drama, is revealed to be a weak, pathetic and puny figure when, accidentally doused with a bucket of water, she dissolves into a steaming puddle...

The victorious foursome return to the great seat of power of the mighty Wizard and claim their promise. Yet inexplicably, he still tries to wriggle out of granting their hearts' desire. Dorothy protests, but her little dog Toto (who hasn't said a word since this whole farago began) seems to spot something, scampers over and pulls away the giant curtain which hides the great Wizard from their wide-eyed gaze. All at once they gasp, as Toto reveals to their horror...

No! Surely the Wizard couldn't be a thief?

And surely the Wizard couldn't be a liar?..

...Or (*gulp*) a scheming sleazebag crook?

...Or (*gulp*) a scheming sleazebag crook?

And the Wizard surely couldn't be a foolish semi-incompetent, entirely devoid of the magical powers he claimed??

At that moment the scales fall from Dorothy's eyes and she realizes that her belief in the power of the Wizard was nothing but an illusion. She suddenly sees that trusting in some external power to rescue her is folly. Still, how ever will she get home?

The Wizard flies off into early retirement in, appropriately enough, a hot air balloon - presumably having pocketed a substantial munchkin bonus - and appoints the Scarecrow, Tin Man and Lion to rule in his place (probably in some kind of coalition).

At which point Glinda the Good Witch reveals that Dorothy, through the magic in her ruby red shoes, had it in her power to escape from Oz and return to Kansas all along - only, before, she never would have believed it! All she has to do is click her heels together three times, and say...

And so Dorothy retuns to Kansas to discover that it was all a horrid, horrid dream. Gradually she wakes to the realisation that the strange creatures she met in Oz were but nightmarish, fantasical projections of the ordinary people surrounding her in her own life.

The Scarecrow, the Tin Man and the Cowardly Lion... the Wicked Witches of the East and West... the empty, blustering Wizard... these were simply the crazy, wonderful, fallible and foibled human beings she comes across every day, blown up into fantasy figures on the screen of her own mind.

But most of all, she comes to learn that looking for solutions to her problems somewhere 'over the rainbow' is a recipe for eternal pain and disappointment; that it's always better to look through illusions and try to live in the real world; and that, most importantly, all the answers she'll ever need will always lie within herself.

The End

~~~~~~~~~~~

WHAT DOROTHY DID NEXT...

So what would happen if we applied some of Dorothy's hard-won wisdom to our current, rather more hum-drum conundrum? Perhaps, if we're able to strip away our own illusions - and those of our politicians - to see the reality of our current plight, we can scruitinize their policies clearly, form a wise judgement and feel confident of making the right choice come May 6th.

So then: in this economic battlefield, what is illusion and what is reality?

Try these three for starters...

Try these three for starters...

----------------

ILLUSION ONE

- Recession, falling house prices and failing businesses are a disaster to be avoided at all costs.

REALITY

- Not only can they not be avoided, they are essential to our long-term recovery.

-----------------

Gradually over the course of the last thirty years, we were seduced into believing we could junk one of the basics of Economics 101: that recessions serve a purpose - to correct the excesses of the preceeding expansion.

We learned to rely upon (and demand) a molly-coddling response from central banks and governments to any crisis that popped up. As soon as there was a whiff of recession in the air, up would step Alan Greenspan to wave his magic wand and - puff! - interest rates would plummet, flooding the world with monetary stimulus.

And lo, credit ballooned with every successive recession, cushioning the effects of increasingly reckless behaviour not only by lending institutions but by investors and consumers. Simultaneously, regulations which had kept the banks from giving in to unfettered greed were gradually whittled away to insignificance under successive governments.

And lo, credit ballooned with every successive recession, cushioning the effects of increasingly reckless behaviour not only by lending institutions but by investors and consumers. Simultaneously, regulations which had kept the banks from giving in to unfettered greed were gradually whittled away to insignificance under successive governments.  But there's an extra, rarely discussed dimension to this story. Underneath all the excessive supply of credit, demand for loans exploded as the massive world-wide baby-boom generation moved into the peak-spending years of their lives in ever-increasing numbers, forming families, buying cars, homes, second homes, renovating, flipping and speculating on them, taking out loans on the back of them, turning extreme houshold debt into another pool of gasoline waiting for a match.

But there's an extra, rarely discussed dimension to this story. Underneath all the excessive supply of credit, demand for loans exploded as the massive world-wide baby-boom generation moved into the peak-spending years of their lives in ever-increasing numbers, forming families, buying cars, homes, second homes, renovating, flipping and speculating on them, taking out loans on the back of them, turning extreme houshold debt into another pool of gasoline waiting for a match.

TOTAL DEBT PER WORKER TRIPLED SINCE 1982

And it's no accident of course that virtually all of this stupendous rise happened while mortgage rates (and interest rates in general) were dropping like a stone...

The upshot of all this is an economy in the western world that, absolutely saturated with debt, requires zero interest rates - not to grow but merely to stop shrinking.

Forget a return to normality, folks. A mountain of excess debt has to be worked off before we even stand a chance of staging a true, lasting recovery.

And this is where that much-maligned institution we call the 'free market' comes in. It may fail us at times of rampant greed, but its efficiency is matchless when it comes to wreaking 'creative destruction'. Left free and to its own brutal devices, it will over time enforce the restructuring and destruction of financial, business and consumer debt.

- It will force companies who over-expanded in the boom years to retrench and restructure, or die

- It will reward smartly-managed companies with increased market-share

- It will punish poorly-managed companies with bankruptcy and the wipeout of bad debt

- It will impel property prices lower to meet reduced demand and reduced mortgage availability, once again making homes affordable to ordinary people as they had always been

- It will punish over-speculation in stocks, commodities and other assets by realigning expectations with reality over time

And so on. Any government attempt to reverse, stymie or curtail this process, to re-inflate the bubble, to prevent falling prices, to artificially or temporarily boost any market which is adjusting naturally to reduced demand, only delays the date at which a lasting and sustainable recovery can finally begin - and creates even more government debt which must be serviced, with interest, by us, the taxpayer.

This is emphatically not a call for a return to fundamentalist, red-in-tooth-and-claw type capitalism; I'm not in any way suggesting we leave the poor and unemployed to grub around in the streets and fight for scraps - who in this day and age could countenance that? I am suggesting that we not allow our fear of economic pain to lead us into grave policy mistakes which in truth merely postpone or prevent ultimate recovery.

-----------------

ILLUSION TWO

By official measures the recession is over - the important thing now is to secure the recovery.

REALITY

It was not a recession - it is a depression. What we are witnessing is the first rebound within a major, structural, long term decline.

-------------------

The closest we have to a widely accepted definition of a 'depression' (it's so long since we had such a thing that nobody ever bothered to come up with one) is a 'fall in economic output of at least 10%'. Well folks, world output troughed at -13% in March 2009; it has since reclaimed less than half that loss and now the most reliable leading indicators of the US economy are slowing once again:

Source: HS Dent, ECRI

The long history of credit and investment bubbles is that, when they burst, they lead to depressionary conditions. Here is Martin Wolf, editor of the Financial Times:

- "First, comparisons between today and the deep recessions of the early 1980s are utterly misguided. In 1981, US private debt was 123 per cent of gross domestic product; by the third quarter of 2008, it was 290 per cent. In 1981, household debt was 48 per cent of GDP; in 2007, it was 100 per cent. In 1980, the Federal Reserve’s intervention rate reached 19–20 per cent. Today, it is nearly zero. When interest rates fell in the early 1980s, borrowing jumped. The chances of igniting a surge in borrowing now are close to zero."

And here's Nobel laureate economist Paul Krugman:

- "I’ve been saying for a long time that this isn’t your father’s recession — it’s your grandfather’s recession. ... That is, it isn’t something like the 1981-82 recession, which was brought on by the Fed to control inflation... Instead, it’s like the 1929-33 recession — or the recession of 1873-1879 — a slump brought on by the collapse of an investment and credit bubble. And monetary policy, at least in its conventional form, has already reached its limits. "

What we're talking about, in other words, is a long-term secular shift in the economy, a reset of debt levels, of spending levels, of growth levels - a process which historically takes years. Here's how David Rosenberg, highly respected former Chief Economist at Merrill Lynch compellingly describes it (from around 8 mins in):

And as the business and banking sectors reset in this 'post-bubble credit collapse', over-indebted consumers will not be dusting off their wallets either any time soon. As I pointed out in my December '09 post, the essential fact which marks out this downturn from all others since the 1930s is that the demographic profile of our society is dramatically changing - and not in a good way.

You'd hope that the greying of the West's population can only lead to a decrease in the level of overall stupidity and a rise in the general supply of wisdom. Alas, it does not lead to a rise in the stock market:

Here is the story of consumer retrenchment in Japan since their own dramatic bust in 1990, super-imposed over Tokyo's stock market index. As the working population aged beyond their natural peak-spending years (46-50) consumer expenditures plunged. This led to falling company profits, dragging down share prices. Brief resurgences through the 1990s would lead to occasional rallies in stocks and flashes of hope for the economy. But the relentless trend was unmistakeable, was predictable and was, indeed, predicted by HS Dent in 1988. The same forecaster, whose demographic model also accurately predicted our '90s boom and the 2008 bust, sees a renewed downturn later this year and continuing crises into 2012; it won't be until the turn of the next decade, he believes, before the real recovery begins.

Here is the story of consumer retrenchment in Japan since their own dramatic bust in 1990, super-imposed over Tokyo's stock market index. As the working population aged beyond their natural peak-spending years (46-50) consumer expenditures plunged. This led to falling company profits, dragging down share prices. Brief resurgences through the 1990s would lead to occasional rallies in stocks and flashes of hope for the economy. But the relentless trend was unmistakeable, was predictable and was, indeed, predicted by HS Dent in 1988. The same forecaster, whose demographic model also accurately predicted our '90s boom and the 2008 bust, sees a renewed downturn later this year and continuing crises into 2012; it won't be until the turn of the next decade, he believes, before the real recovery begins.Japan loaded up on government debt to fight their slump and enacted endless stimulus programmes (I believe it's eight by the latest count), yet only succeeded in digging itself further into the mire; it now appears incapable of acheiving strong growth in its present bloated state.

The crucial lesson, then, that any prospective government must take from this - and that we voters must seriously take into account too - is that short term measures designed to stimulate the economy are doomed to failure. Not only that, but if they lead to increases in government debt, the resulting higher taxes will weigh down our economy, make even more subdued those occasional rebounds which would otherwise occur, and leave us unable to take advantage of the upturn when it eventually comes.

And finally...

--------------------

ILLUSION THREE

The choice we face is between a steady recovery under the 'XX Party' and a double-dip recession under the 'YY Party'

REALITY

The true risks for either party lie between a renewed downturn with high interest rates and a renewed downturn with low interest rates.

---------------------

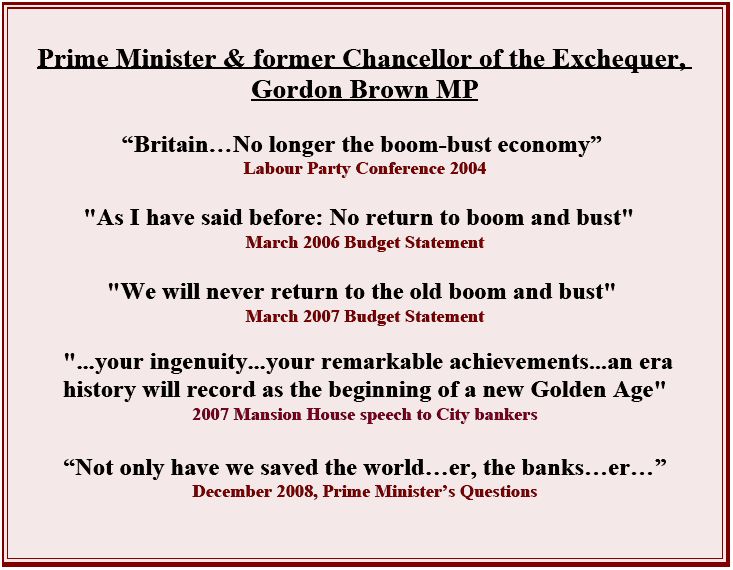

OK, I accept he may have numerous admirable qualities, but what I really cannot forgive Gordon Brown for is his failure as Chancellor to foresee or to prepare for even a modest downturn in our economic fortunes.

Government borrowing rose steeply into 2007, as he spent like water on public services and saw no need to cut the level of government debt. But you didn't need to believe as I did that a depression was coming to wonder if the good times could really carry on in perpetuity as he ("we will never return to the old boom and bust!") seemed to assume. Don't you think a sensible steward of the economy would have used at least some of the past decade's unprecedented bounty of growth to fix our financial roof, pay off some of the debt and prepare us for that inevitable rainy day?

But Gordon fell into the classic trap of those who've been in power too long: he began to believe his own propaganda.

Recently he has continued to, shall we say, flambé the statistical actualité in front of the Chilcott Committee on Iraq and in a recent speech on immigration. Surrounded for so long by sycophants, he seems to have been overcome by a sense of infallibility in which he subconsciously assumes that, because he says something, it must be true. Happened to Margaret Thatcher, happened to Tony Blair. Hmm.

So far, so psychobabblogical, but the consequence of his hubris was real: thanks to the devastation wreaked by the financial crisis and the vast sums thrown at the banks, he has left us with a government balance sheet hock deep in debt with absolutely no room for manoevre, and an incoming government which has to slash to the bone the very services Brown (and we!) worked for ten years to improve - all to avoid a catastrophe in the bond markets.

BE IN NO DOUBT: THE BOND MARKET IS NOW IN CHARGE OF OUR FATE

We are, more than at any time in modern history, now dependent on the largesse of the big institutions who buy our government bonds (gilts). The $83Trillion international bond markets are absolutely not to be underestimated, as previous Chancellors Denis Healy and Norman Lamont discovered to the permanent cost of their reputations.

Understandably, many commentators have been won over by Keynesian arguments which insist that governments must spend liberally in recessions when everyone else is cutting back. This makes economic sense when a government's finances are in good shape, but when they are not, you're flirting with disaster. Here's Derek Scott, former economic advisor to Tony Blair, who worked in the Treasury back in the dog days of the 1970s:

- "It is very serious. There is an argument over whether you should cut the deficit at a time when the economy is weak. I think that argument is stronger if you'd gone into the recession in a much better financial postition. My own experience, working for Denis Healy many years ago is that the longer you delay the action then the more draconian it has to be, and when you take the appropriate action it's quite surprising how quickly confidence can be restored. So I think there has to be a fairly sharp and early tightening of policy. There is some risk that that does slow the economy down but frankly I think that's less of a risk than doing nothing and finding the bond market's slowed your economy down and in a much more dramatic way." Sky TV 'Jeff Randall Live' April 2010

There is a good case for spending what we can afford on very long-term investment projects in areas like energy and education which will pay us back in growth over decades and create jobs long after this crisis is past.

But right now, our finances are in a state comparable to that of many of the so-called 'PIGS', in terms of our budget deficit and overall level of debt (see January's post for gory details).

Unlike them, however, we do have one supposed trump card - we can print our own money.

And that means we won't technically default, because we can always pay our debts by creating money out of thin air. But if we end up having to do that, thus devaluing our currency, there's a price to be paid - and it's in the bond markets.

Here's what happened to the price the wretched Greeks have had to pay the bond boys in order to finance their profligate spending.

Here's what happened to the price the wretched Greeks have had to pay the bond boys in order to finance their profligate spending. If this happens to us, we're cooked.

Not only will interest rates on government debt shoot up (making a trip to the International Monetary Fund a nailed-on cert) but, because of the linkages throughout the system, interest rates generally including mortgage rates would also rise. Many people would be unable to afford a sharp jump in their repayments which, in combination with a renewed rise in unemployment from another round of business loan defaults, would see the great orbiting space ship which is our housing market begin its long-anticipated return to earth.

So when both George Osborne, the somewhat ghoulish and otherwise wholly unconvincing Shadow Chancellor, insists we have to tackle the debt immediately and Derek Scott, long-suffering Labour economics guru, says we should tackle the debt immediately, these are the very real risks they are talking about.

It is not any more in the gift of our government to decide whether and by how much we reduce our debt. If we do not make convincing moves soon, the price of that debt will rise and our toilet-paper-thin recovery will be flushed down the Tony before Gordon can say "maybe winning this election wasn't such a good idea after all."

--------------------------

CONCLUSION:

WHO WOULD TOTO VOTE FOR?

So Dorothy, as you stand in that rickety old booth on May 6th and carve that X with your little tethered pencil, ask yourself who Toto would vote for; don't give in to illusion, and steel yourself to see the world as it is -

Let market forces work: re-inflating the bubble is not an option and any effort to do so will hamper recovery in the long term

Short-term fixes are useless, wasteful and counter-productive in a depression, but targeted long-term investment will help

Cutting government debt is not now an avoidable inconvenience

This does not mean we must vote to abandon compassion for those caught in the inevitable fallout. If anything, compassion in government policy will become more important than it has been for a generation. But our government will have to learn how to strengthen the precious safety net and invest in major long-term projects without bankrupting the nation; it will finally need to achieve more and spend less.

Can we all vote for that?

Can we all vote for that?

--------------------------

Well, I'm Totoed. After such a marathon post, there'll be a brief delay in delivering this month's Investment Outlook, which will appear this Tuesday 7th April as we approach another important turning point for the markets.

On the Money meanwhile will return with a post-election post-mortem post, on Sunday 9th May.

Spring's sprung - have a great month!

Spring's sprung - have a great month!