Whatever you do, don't look up

Evidence is accumulating that the recent breakout to new highs in many world markets may have been nothing but a giant head-fake.

As investors' bullishness soared to multi-year highs, to levels which have consistently led to a sell-off over subsequent months, the hoopla around the launch of QE2 by the Federal Reserve encouraged many to believe that markets were impervious to downside risk.

Trouble is, if everybody minded to buy has already bought, prices will peak no matter how much QE cash is swilling around.

And as I mentioned a while back, there was always the possibility that investors, in anticipation of the Fed's move, had already priced most of its impact into markets in the months between Bernanke's heavy hints in August and early November when the formal announcement was made.

What's more, the Fed announced the programme would probably end in June. Investors saw this summer what can happen when the Fed zips up its wallet and the market is left to fend for itself, so those who think that's likely to happen next summer will at some point, perhaps come spring, begin to sell risk assets in anticipation of the withdrawal of Fed stimulus.

Meantime, those smarter traders who bought the rumor months ago are busy selling the news and, as ever, it's the 'dumb money' that's buying up the scraps.

INVESTORS' INTELLIGENCE?

HMM...

Alongside the previously noted American Association of Individual Investors survey (still wildly bullish), the most long-standing and reliable measure of ordinary investor sentiment comes via the weekly Investors' Intelligence survey of newsletter writers, which has a history stretching back four decades.

Sadly, despite its name these investment advisors have a time-tested track record of encouraging their readers to buy at the top of major moves and sell at the bottom. A very few of the hundreds surveyed have stellar records, but as a group these advisors have proved a remarkably reliable contrary indicator for those of us who would rather buy low and sell high.

Last week, newsletter writers became more bullish than they've been since the market topped in October 2007.

Sentiment expert Jason Geopfert has taken a look at their record when they've become this bullish only after an 18-month bull market run such as we've had. Going back to 1969, there have been just eight discreet periods when they became this excited so late in the day - all were a clear signal either to sell or steer well clear of stocks.

I've highlighted them on the following charts of the Dow. It's worth noting that most instances occured as the market was breaking out to a new 52-week high (which we just did) and that, once the market then began to pull back, it marked an important peak looking out over the next few months. A couple of instances were at or very close to long-term tops, while the rest held for anything from two to nine months before pushing higher.

In every case, however, the Dow was either flat or substantially lower 18 months later.

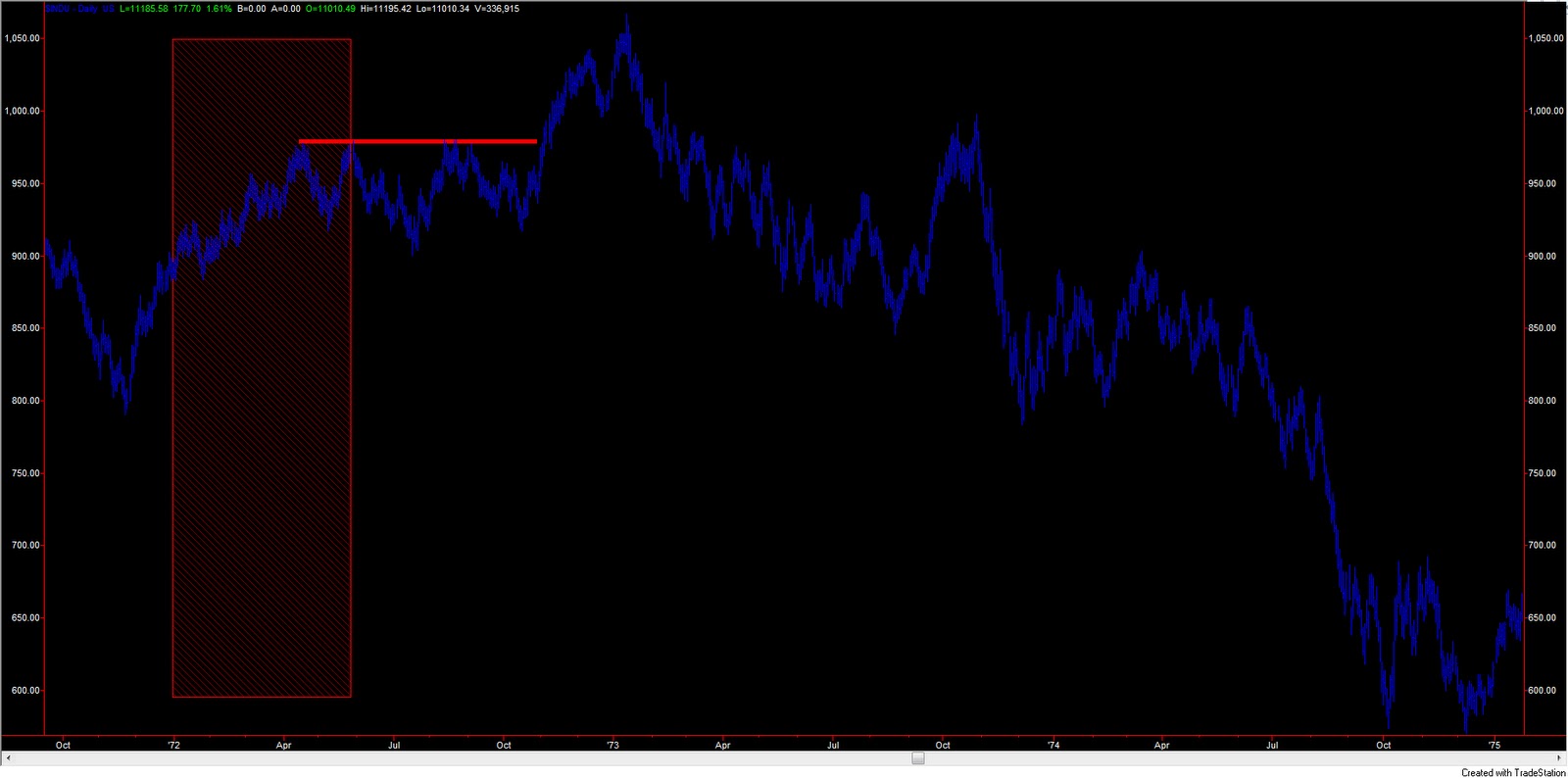

INVESTORS' INTELLIGENCE BULL RATIO* HITS 73%+ FOR FIRST TIME AFTER 18-MONTH RALLY FROM A MAJOR LOW

1972 - 74

|

| Click chart for monster-size graphic... Newsletter advisors became 73% bullish at the beginning of 1972. In April, the Dow hit a new 52-week high (horizontal bar) - a top which held for six-months. A head-fake rally into 1973 then marked the start of a terrifying 50% decline. |

*Bull ratio = Number of bulls divided by (total bulls + bears)

1976 - 78

1986 - 88

2004 - 06

2006 - 08

The charts rather speak for themselves. They also chime with any number of other studies I've looked at recently, as well as my own major momentum study, which suggest we're in for either

- a choppy sideways-to-down correction lasting at least two months but possibly up to one year, followed by a breakout higher, or

- A major top

NO SAFE HAVENS, MURIEL

The picture for precious metals, oil and other commodities is similar. Historic levels of sentiment noted in a previous post only worsened as prices ramped up recently, and despite a nasty correction over the past week that has barely changed. Barring a major sovereign debt crisis which propels investors into gold, my view remains that, after perhaps one more push higher, the party will finally be over for commodities.

That will have a major impact on a number of potential investment vehicles -

- Emerging markets dependent on exports of raw materials such as Brazil and Australia will endure a heavy hangover. If China slows further (see below) it could be a body blow for many Asian and Aussie exporters. If that downturn raised unemployment it could finally break the back of the Aussie housing market.

- The international mining and oil companies which make up so much of the FTSE 100 will suffer and drag the index down with them.

- A peak in commodity prices may also coincide with a building peak in China, which is suddenly struggling with a serious inflation problem and is having to slam on the brakes. Wanna take odds on China avoiding a property crash now?

ON THE MONEY...AGAIN (Yawn)

Yet if this picture of commodity weakness is to be realized, it will surely need to coincide with a significant bottom in the US dollar, as I strongly suggested in a piece last month. Unfortunately, just as I was preparing my November On the Money post two weeks later, the plunging greenback began to make me look like an imbecile: it was getting flushed down the swanee as almost every 'expert' and TV pundit had sworn blind it would. It seemed I was dead wrong.

Then a funny thing happened.

Then a funny thing happened.

As soon my post appeared, the dollar decided it had taken enough punishment and shot higher. Take a peek at the chart. It seems that, unless the buck collapses from here, my contrary call might have been on the money after all.

And that's why this blog sits snugly in your favourites list*, doesn't it gentle reader?

|

| A textbook case of 'no one left to sell' |

*There are many (excellent) financial blogs which deliver a constant stream of posts every day. Mine's not one of them. I'll only update when there's something really important to say, or when there appears to be a significant market turning point ahead. Get these occasional but essential updates, plus my OntheMoney monthly opinion piece, by email direct to your inbox. Subscribe scot-free at the top of the page...my God, what a steal.