You've seen this movie before

Ever wished you could do something utterly selfish, wicked and outrageous and never have to pay the price?

Ever wanted to stuff your face with unctious cream cakes knowing that you'll weigh no more tomorrow than you did today? Ever wished you could punch your obnoxious work colleague in the gob with absolutely no comeback? Or how would you like to spend the night making mad passionate love to a complete stranger - then erase their memory of you overnight so you can seduce them all over again?

Well, for anyone who wants to put their money in the stock market, watch it soar in value, then just as they've loaded it up with all their savings see it once again crash, burn and reduce to a pile of worthless, smouldering cack - welcome to GROUNDHOG DAY, directed by and starring Ben S. Bernanke, Chairman of the US Federal Reserve.

In Harold Ramis's inspired comedy, a sour TV weatherman played by Bill Murray finds himself literally reliving the same day over and over again. Every day he wakes at 6am sharp on February 2nd. Every day he finds himself in the same awkward situations, insulting the same weird people, repeating variations of the same hideous mistakes. In his desperation, he finally kills himself - only to wake up at 6am and start the whole day over again. He just can't stop screwing up. It's Groundhog Day.

Well folks, the Federal Reserve and its love-children in the banking, trading and investing community who have learned to suck on its fulsome teat, are now engaged in a rinse-repeat cycle of the same catastrophic mistakes which led us into this crisis in the first place; mistakes which led directly to the creation of two of the biggest bubbles and crashes in financial history, a wipeout of trillions of dollars of household wealth and a cratering of the world economy.

I had intended to use this month's post to take a positive look at where we could best park our hard-earned to find a decent return over the next few years. But in light of the Fed game-changer, I've decided to postpone that for a couple of weeks because the major implications for our economy and investments are worth a timely examination.

In this post, I'll conduct a brief but thorough strip-search on the likely effects of Uncle Ben's free-money deluge, and offer some thoughts on how we can best survive it. We'll discover how years of such interventions have led us into a series of ever-greater crises, find that we can loathe the Fed and all its works but still make money as we loathe, and see how we can be primed and ready for the eventual reckoning whenever it comes, as it surely and inevitably will.

__________o0o__________

QUANTITATIVE EASING:

THE FACTS

THE FACTS

There's much hokum and hyperbole surrounding this policy, and there are plenty of financially savvy people who talk complete cobblers about QE, so let's pin down exactly what the dang thing is before we get into its rights and wrongs.

- IT'S NOT PRINTING MONEY - IT'S A SWAP OF CASH FOR BONDS

A lazy way of describing QE is to say the central bank simply prints money and pumps it into the system. To my shame I have been guilty of using this shorthand myself, but it is actually a distortion of the truth.

When you decide to sell your holiday home in the Seychelles, you offer it up for sale. If I buy it with cash, you lose the income and capital value of that asset, but gain the cash value you've agreed with me. You become, as they say, liquid, and can now go forth and spend that money on another palatial mansion in the Cayman Islands (or on a lock-up in the Isle of Dogs). Or you could plough it into stocks. This is what happens in QE. The Fed electronically creates credit in its own reserves, then uses it to buy an existing asset (such as a government bond or mortgage-backed security) from one of the major banks, the so-called Primary Dealers.

- INSTEAD OF BONDS, BANKS NOW HAVE THAT VALUE IN CASH AVAILABLE TO PURCHASE MORE ASSETS

Through a procedure known as POMO (Permanent Open Market Operations) the Federal Reserve (or Bank of England or whoever) buys the bonds electronically, substituting cash to the value of an agreed price; that cash now sits in the Primary Dealer's reserve account at the Fed, and receives a piddling amount of interest just like an ordinary current account. The P.D. is then free to utilize this cash to lend or invest as they deem fit.

QE therefore increases the bank's liquidity - its available cash - but does not increase the total asset value on its books, nor does it increase the total amount of assets in circulation in the real economy. The bonds themselves are now out of circulation and sitting in the Fed.

- THE BANKS CAN HOLD ON TO THIS CASH, DRAW ON IT BY LENDING OUT TO BUSINESSES, OR USE IT TO SPECULATE IN FINANCIAL MARKETS

According to the Fed, $600 billion of QE will be used to buy government bonds at a rate of $75b per month until the middle of next year. Much of this, they believe, will not be hoarded but used by banks to lend and speculate. Which brings us to another associated 'benefit' of QE:

- THE PROCESS OF MASS BOND-BUYING SHOULD LOWER INTEREST RATES

This, says the QE crew, is one of the policy's most important boons. Since a bond's price moves in the opposite direction to its interest rate, when the Fed buys so many bonds (and others buy on their coat-tails) the effect, at least according to theory, is to push prices up and force rates down.

So in these two ways - through lowering lending rates and encouraging banks to utilize that cash in the economy - the central bank is hoping to stimulate overall demand. It wants to see more lending, spending and speculation. It wants to see banks lending to companies, it wants interest rates to fall which should encourage risk-taking by borrowers, it wants to reduce the price of exports by devaluing the dollar, and it wants to boost asset prices, lower savings rates and encourage consumer spending. That's all it wants.

Dear reader, this is the theory of QE and whether you or I approve of it or not is by the by - it's coming soon to a mega-bank near you. Only three questions worth asking remain:

- Will it boost lending, spending and / or speculation?

- How do I gain if it succeeds?

- How do I gain if it fails?

Let's take a look.

LENDING

BANKS TO MAIN ST: "SIT ON THIS"

As we all know, renewed lending and higher spending are essential if we're to create jobs and get things moving again. Trouble is, when we check the facts on lending there's no evidence that QE, wherever it's been tried, has made banks inclined to lend a penny more.

There have been three modern-day iterations of quantitative easing - the $1.75 trillion US shock-and-awe programme from early '09 to early '10 (let's call it USQE1), the UK's $200bn equivalent over roughly the same period (UKQE1), and Japan's initial QE experiment from 2001 - 2006 (JAPQE1).

Here's the lending picture for USQE1:

The period of Fed intervention lasted from just after the peak in lending at the top right of the chart, right through to the trough in March 2010. If you didn't know better, you might suppose QE has a negative effect on bank lending rather than a positive one. Is the UK picture any brighter?

|

| Source: Bank of England |

The programme began in January '09 and ended in February '10; overall lending dropped precipitously from the get-go and has slid pretty consistently ever since.

|

The picture is particularly bleak for small and medium-sized businesses where most job growth normally comes from. Zero encouragement, then, from the latest QE attempts - how about the original, the Japanese experiment in 2001?

|

| Inflation hawks freaked over the expansion of base money during JAPQE1 (which includes bank reserves), but the real story was the blue line, the plunge in lending. |

|

| Loans to the private sector (white bars) slumped during Japan's QE |

QE did not encourage lending, even after the end of recession in 2003. It becomes even more stark in this graphic from a report by Japanese economist Richard Koo, which shows the only expansion in demand during QE came from the government - lending to private businesses shrivelled, then flattened by 2006.

The very best we can say from these instances is that QE had no discernable positive effect on lending behaviour. Perhaps there would have been even less lending without it, but of course one can never prove a negative. We do know for sure however that, courtesy of QE1, the banks have a truly mind-boggling amount sitting in reserves should they wish to use it for lending - and so far they certainly ain't.

|

SPENDING

YOU CAN LEAD A HORSE TO WALMART, BUT YOU CAN'T MAKE IT FLASH ITS GOLD CARD

We know that business spending recovered fairly well after its cliff-edge fall in '08 and early '09, largely as a function of the need to replenish inventories run down during the recession. But what next? A business decision to invest substantially in new facilities or hire more workers does not occur on the whim of an executive after a boozy lunch, but in response to a sustained increase in demand for their products...

|

| Source: Goldman Sachs |

It is growth in consumption that will fuel business spending, not cheap money from the Federal Reserve. So let's make a careful inspection of the elephant in the room - the consumer.

The lightest green line is this year's spending level. Along with last year's, it has essentially reset massively downwards from the debt-fuelled consumption of the pre-credit crisis era as shown by the dark green line. However, there is a gradual trend of improving spending from March '09 to May 2010, which has since receded.

This pattern of a spending rebound followed by a dip is also clear in the figures for UK retail sales:

|

| UK retail sales 2009 - 2010 Source: Office for National Statistics |

So consumer spending picked up during the period when QE was in effect, then fell back after it ended early this year: is there a link?

There certainly hasn't been a splurge on consumers' credit cards or a boom in personal loans...

There certainly hasn't been a splurge on consumers' credit cards or a boom in personal loans...And it's not as if there's been a sudden boost in wages either...

|

| Stagnating / falling wage growth during QE |

|

| Source: Tradingeconomics.com |

|

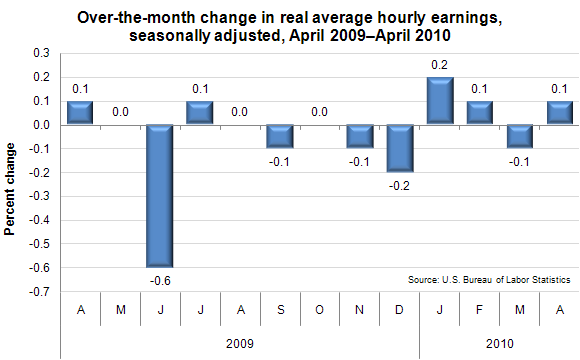

| Stock market moonshot during QE1, March 2009 - April 2010 |

Could it be that consumers, pulling out their 401k and investment statements, are looking at the remarkable recovery in their retirement accounts and taking it as a green light to go out and spend?

If that is in fact the case, it couldn't be, could it, that our central banks are deliberately fuelling a speculative stock market boom with QE to encourage more consumer spending? Boosting market prices to create a 'feeling' of greater wealth and confidence, even if the true economic picture does not support it? In effect, putting the cart before the horse?

Gentle reader, yes. Incredibly, they are.

SPECULATION

FED TO WORLD:

"BUY STOCKS - THEY CAN'T GO DOWN"

I'm no conspiracy theorist. Do n0t get me started on JFK, MLK, the military-industrial complex or the moon landings. 'Obama's-fake-American-passport' nutbags are not welcome in these fantasy-free rooms.

However.

It had been an unspoken assumption of many market observers for years that the Fed was actively engaged in supporting the stock market, especially in times of crisis. Technical conditions would have traders expecting a serious downdraft when, seemingly from nowhere, the market would suddenly find a bid and shoot higher.

Nobody could ever prove such a mechanism existed. Traders imagined some kind of Black Ops team, based in a high-tech bunker somewhere behind barbed wire in the depths of open country; a kind of Men In Black setup, ready at the touch of a button to inject $trillions in cash and put a floor under stocks when the ice got a little too thin. True believers called this mysterious operation the PPT - the Plunge Protection Team.

Now we finally know the truth. It really really does exist - except, it's not a secret. It's not a covert operation. It's happening in plain view and has, as its Black Ops team, a massed army of traders in the world's major banking institutions. It turns out, in fact, that the operation is run by this man:

|

| NOTORIOUS |

Look, I never really bought the whole PPT shtick. But this is different. Not only is it clearly in the interests of Bernanke and the Fed to artificially boost stock prices, they now openly admit that is what they're doing.

THE WEALTH EFFECT &

HOW IT CORRUPTED A NATION

Last week in the wake of his announcement the notorious VIG wrote a justification of his actions in the Washington Post. In it, Bernanke opined:

"...Higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending. Increased spending will lead to higher incomes and profits that, in a virtuous circle, will further support economic expansion."

Now Bernanke is no trailblazer here - he is merely maintaining a venerable tradition. His mentor and predecessor at the Fed Alan Greenspan is the true godfather of this policy, which had its genesis in the great stock market crash of 1987, when a rookie Chairman Greenspan found his first taste of success opening Fed spigots in the face of a crisis.

In a remarkably revealing TV interview earlier this year, Uncle Alan spoke about this 'wealth effect', why he is so enamoured of it and how he believes a falling stock market is the spawn of the devil and a booming market cures all ills. From this belief, it is now clear, current Fed policy sprung.

Between the lines, his message is clear: get cheap money to the banks by any means necessary and set them loose to bid up asset prices.

And in a far more blatant admission Brian Sack, the unfortunately-named head of the operation which actually conducts the Fed's bond purchases ('POMO'), gave a speech a few weeks ago which left traders and commentators slack-jawed. In a moment of brazen candour, Brian let the cat right out of the...er...sack.

"QE", he insisted,

"adds to household wealth by keeping asset prices higher than they otherwise would be."

Yes, fellow traveller, you read that correctly. Asset prices, by implication, should be lower. The Federal Reserve is, as a matter of policy, artificially boosting the value of the stock market and in doing so is attempting nothing less than a bald-faced confidence trick.

Even if the economic fundamentals do not justify higher prices, they are ensuring that markets will be inflated in order to create an impression of wealth, thereby giving an inducement for investors to spend these 'gains' and make the economy play catch-up. It is the definition of putting the cart before the horse, maxing-out Uncle Ben's platinum card in a conceit entirely befitting the credit-addled age in which we live.

If you still cannot believe the Fed could or would artificially goose stocks, a number of recent studies have gone over the official data from Fed POMO operations during the past five years and proved the overwhelming effect of their interventions beyond a shadow of a doubt.

|

| The only annualized returns from stocks over the past five years have come from days (blue) when the Fed intervened - incredible. |

THE WEALTH EFFECT IS REAL -

BUT SO ARE ITS CONSEQUENCES

|

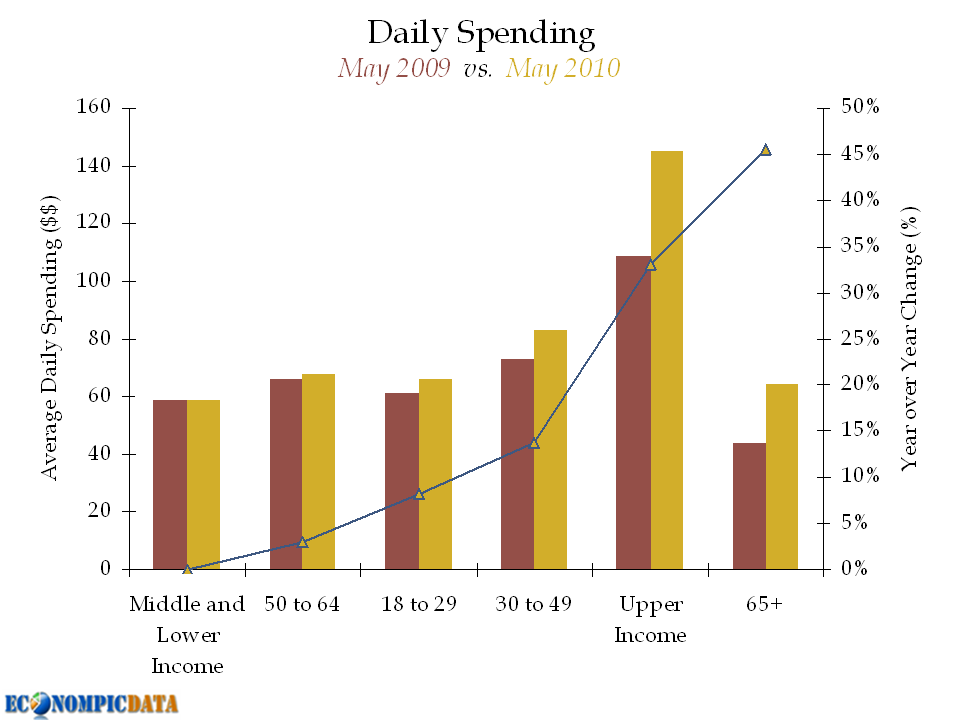

| Upper income earners - those with greatest gains from rising stock prices - did boost their spending during QE1, but those on middle and lower incomes did NOT |

Don't get me wrong. Academics have noted a 'wealth effect' in the economy for years; there's no quibbling that higher asset prices (stocks, houses) do encourage people to go out and spend, even though the effect is often fairly small. But using the wealth effect as a policy tool is something else entirely, an enterprise with consequences totally lost on Bernanke and his ivory-towered men in grey:

You cannot encourage people to believe that an asset class is sure to rise in value without creating the conditions for a self-sustaining bubble. As all bubbles eventually burst, those same people you have been encouraging to speculate and spend will see their new-found 'wealth' erased in the ensuing crash, either directly, or indirectly through a subsequent economic recession.

This objection is hardly new. The self-same policy - flooding the markets with liquidity at the first sign of trouble - is widely acknowledged to have created conditions which led to two market meltdowns and recessions in ten years.

GROUNDHOG DAY ALL OVER AGAIN

The trouble is, Bernanke has never shown any appreciation or understanding of the dangers of financial bubbles. This is quite clear from any number of his writings and the woefully naive reaction he showed to the housing boom, a situation which, even in the mid-2000s, was plainly a bubble to anyone with eyes to see.

(Warning! - beware of flies, as some sections of the following video may leave your mouth agape.)

Greenspan formulated and perfected the stock market bailout (the aggressive slashing of interest rates followed by tiptoeing rises) through a number of crises, beginning in the '87 crash and continuing through the 1991 recession and Savings & Loan crisis, the 1997 Asian contagion, 1998 Russian default, 1999 Y2K scare and the 9/11 panic of 2001. Even that briefest and mildest US recession of 2001 was met by a slashing of rates to 1%, a level maintained for more than a year as homeowners, flippers, speculators and banksters built up a head of steam in the housing market.

Now, with QE2 launched even as the economy shows signs of stabilizing, Bernanke is at it again. Here's how David Stockman, former budget director under Ronald Reagan, memorably describes it (from around 1min in):

THE SPIRIT OF THE TIME

Let's be honest, the Fed's behaviour is hardly surprising given the world in which we now live. The need of investors for instant gratification, their desire to avoid solutions which require loss-recognition or even temporary pain and the fear of even asking for such sacrifice by politicians and policy-makers, reflects a general societal malaise one might characterize as the 'spirit of the time'.

French economist Didier Sornette, in his 2008 paper on Financial Bubbles, illustrates the gap between our fantasy-wealth and reality with this chart comparing real wages in the advanced economies with consumption. Until the mid-1980s, one was enough to support the other. But globalization, competition and rising productivity meant wages soon began to stagnate even as consumer appetites soared - a gap which could only be replaced by debt, including the extraction of profits from rising home and stock prices.

Beyond a certain point, bubbles would form and this asset-price wealth would inevitably become illusory. But each time realization dawned on investors and markets plunged, Greenspan / Bernanke knew that they could revive the illusion with monetary policy.

In the absence of real productivity gains leading to real rising wages, the boosting of asset prices to enable continuing 'wealth-extraction' was the only alternative to major collapse. In 2008, that reality check could no longer be avoided; yet here we are, attempting to re-blow the bubble once again.

The more one considers it, the more this policy begins to resemble a classic Ponzi scheme. Sornette puts it succinctly:

SPECULATION -

THE ONLY WAY QE2 CAN POSSIBLY 'SUCCEED'

So here's what we've found: if previous examples of bank behaviour during quantitative easing persist, lending into this bombed-out economy is not likely to pick up anytime soon, since banks can make their profits elsewhere (by speculating in bond, equity and commodity markets at lower risk).

And if business behaviour persists, corporate investment and job growth is highly unlikely to pick up until consumer demand rises. Yet what increase in consumption there's been in this post-recession funk has not come from middle-income earners or from real wage growth, but from high-income earners soothed by the revival of their 401ks and investment accounts.

The 'success' of QE2 will therefore depend on asset values continuing to rise, fuelling the wealth effect. The speculative bubble now being unleashed in this Fed-induced euphoria already carries the seeds of its own destruction - crippling oil and commodity prices - but the bubble may take some time yet to burst. And this brings us to the most important and challenging question:

WHETHER QE2 SUCCEEDS OR FAILS,

HOW DO I GAIN ?

After my diatribe, you might imagine I'd want to poo-pooh this market rally, sell into it, or even go short. Not so fast, gringo.

I may be a QE2-skeptic, I may be stubborn, but I'm no masochist. When it comes to pounds, dollars and sense I prefer the Ned Davis approach captured in the title of his 1999 book: 'Being Right or Making Money'.

As long as the major banks and their trend-following bag-carriers in the world's large financial institutions are bidding up prices with Ben's blessing, markets are doomed to rise whether any of us like it or not. Not in a straight line, not without hiccups, but the history of POMO ops from 2005 on suggests risk assets are highly unlikely to suffer a fall of any significance as long as the Fed keeps the taps on and the economy holds up.

There is however another risk to rising stock and commodity prices: an exogenous shock such as a sovereign debt crisis in Europe, for example or a collapse of the housing market in China, or even more major home price declines in the US, all of which I regard as high probability events. What we need, then, in the face of these mighty cross-currents, is a serious strategy. Phew - here's one just in time.

A SERIOUS STRATEGY

Over the next couple of weeks I'll be finalizing my long term investment strategy, a simple-to-operate but systematic and historically highly successful approach I began detailing in posts here and here. Since May it has been in cash and inactive. However, in line with my research, if the S&P500 closes out the month of November above its April peak at 1219.80, it will be time to get serious again about buying. Watch this space.

Meantime, the asset classes most likely to do well may be the riskiest. Technology, small-cap and emerging market stocks; industrial commodities feeding the incessant Chinese construction treadmill, oil, copper and the 'anti-dollar' trades, gold & silver.

Yet all these trades are already extremely crowded and investors may find themselves banging their heads against a sentiment ceiling very soon. A major reversal in the dollar will sound the death knell for this approach.

One reason I expected a serious correction until recently was that sentiment had become very heady. The situation is now even more extreme. Everyone believes stocks have to go up. So while it may be tempting to pile in here, I'd be careful as prices may be compelled to pause or pull back before long. In this environment it's as well to remember Bob Farrell's Rule of Investing No. 9:

'When all the experts and forecasts agree, something else is going to happen'.

__________o0o__________

WE'VE SEEN THIS MOVIE BEFORE -

WE KNOW HOW IT ENDS

In Groundhog Day, grumpy old cynic Bill Murray goes through hell, repeating the same mistakes ad nauseam until he finally works out how to live his day generously and treat people well - at which point he wakes up the next day to start a new life. It sounds cheesy I know but the film is so funny you end up swallowing the message whole.

In our economic equivalent, with Bernanke apparently determined not to learn from the Fed's previous errors, it seems inconceivable to me that his experiment could end well. None of the problems which dragged us into this pit in the first place - principally the astronomical debt levels and the housing dog-mess - have been remotely resolved and demographic headwinds will work heavily against Ben's best attempts to get consumers to open their wallets.

In any case, don't we really need to make tapped-out consumers save more and pay down their debts? The whole policy is utterly bankrupt.

|

Nevertheless, on the way to being proved right eventually, I have every intention of making money. So flexibility will be key here within the long term strategy I'll update you with in a few weeks. (Don't forget, you can get a link to any updates automatically emailed to your inbox as soon as they're posted; just subscribe using the button at the top of the page).

Until then, my long-suffering reader, or until we meet again on Sunday December 5th when I hope to tickle you with a much more festive post,

Thanks for stopping by and have a great month!